当前位置:网站首页>Development of trading system (I) -- Introduction to trading system

Development of trading system (I) -- Introduction to trading system

2022-06-25 03:58:00 【Tianshan old demon】

One 、 Introduction to transaction process

A The stock market , Investors must go through the brokerage company's trading counter to connect to the exchange , That is, the trading order is sent from the customer strategy server to the trading counter of the brokerage company , After internal processing at the trading counter, it will be sent to the exchange , The exchange will send the return to the trading counter after confirming the order , The time-consuming of the overall link from the counter to the client policy machine .

The link between the report to the exchange and the return to the policy server is the same .

Two 、 Securities trading solutions

- Introduction to securities trading solutions

A complete stock exchange includes an exchange 、 Buyer 、 seller , The architecture of the securities trading solution is as follows :

2、 seller

A seller is an entity that packages various assets into products and provides them to the market , Such as major securities companies ( Citic securities, 、 Citic built for 、 Haitong securities 、 Guotai Junan Securities, etc )、 Futures companies ( Yong'an Futures ).

3、 Buyer

The buyer is the entity that manages the investment , Such as public funds 、 Private equity funds 、 Hedge funds 、 The insurance company 、 Individual investors .

4、 supplier

Suppliers are manufacturers that provide business solutions for buyers and sellers , Such as Hang Seng ( Public offering fund )、 Kingstar ( futures )、 Gold card ( negotiable securities )、 Communication ( Online trading )、 flush ( Online trading )、 Great wisdom ( Personal information )、Wind( Securities trading 、 information ).

3、 ... and 、 Exchange trading system architecture

1、 The shenzhen stock exchange Business architecture of trading system

2、 The shenzhen stock exchange Trading system architecture

3、 The shenzhen stock exchange Trading system network architecture

The network structure of the trading system of Shenzhen stock exchange is as follows :

4、 The shenzhen stock exchange Trading system features

(1) Integrated trading services

(2) Diversified business services

(3) Flexible and extensible access services

(4) Efficient market service

Support 0.5 second 1 Round snapshot of the high-speed market

(5) High availability

(6) High performance

(7) Low delay

(8) High capacity

(9) Easy to expand

Performance and capacity levels are easy to scale :

Flexible support for new products and new businesses :

5、 The shenzhen stock exchange Trading system interface

(1) At the same time, it provides two interfaces that are faster and easier to expand , Users can choose STEP Interface 、 Binary interface .

(2) File exchange interface , Support XML file 、ETF PCF file .

(3) New gateway based on new interface , Such as transaction gateway 、 Market gateway 、 File gateway .

(4) Basic data expansion

6、gateway brief introduction

A trading unit is a member ( securities company ) Applying to the exchange for establishment 、 Basic business units involved in securities trading and receiving supervision and services . Members can , Apply to the exchange for the establishment of one or more trading units ; Different members may not use the same trading unit . The exchange manages the business of its members through the trading unit , According to the business license scope and application of the member , Open or restrict the transaction authority of the transaction unit according to relevant business rules .

Gateway refers to the gateway placed at the member 、 The software and hardware facilities used to connect members with the exchange trading system . Members can offer through multiple gateways at the same time , However, it is not allowed to use other people's gateway to offer . Members can configure subordinate transaction units on the gateway as needed . Multiple transaction units can be configured on one gateway at the same time , One transaction unit can also be configured on multiple gateways .

The exchange controls the total amount of the offer flow rate of the members through the gateway . When the actual offer rate reaches the flow rate limit of the gateway , The throttling function is on , Offers exceeding the limit will be postponed to the next period of time . Members can apply to set the offer flow rate of the gateway according to their needs . Shenzhen Stock Exchange stipulates that each standard flow rate is 50 pen / second . The flow rate configured to the gateway must be an integral multiple of the standard flow rate . At present, the maximum flow rate supported by a single gateway is 1000 pen / second . The exchange will test and adjust the standard flow rate every year , Ensure that the overall flow rate owned by members meets the needs of market development .

Transaction participants ( securities company 、 Fund company, etc ) You need to connect to the transaction gateway 、 Market gateway 、 File gateway .

Level I Market users ( Pure market users , High single user ) Need to connect to the market gateway .

Level II Market users ( Information service providers ) Need to connect to the market gateway 、 File gateway .

The fund custodian bank needs to connect to the transaction gateway ( Receive transaction data )、 File gateway ( As required )、 Market gateway ( As required ).

7、 Transaction gateway

The knocking mechanism of transaction gateway takes the platform as the unit , Different platforms knock on the door independently every time the platform changes from the non open state to the open state , The transaction gateway measures the network delay between the gateway and the matchmaking engine , And collect ( And only ) The first commission of the counter , According to the network delay, the platform shall be opened in advance ( Ahead of time = Network delay ) Report and knock , If the knock is successful ( That is, the declaration is accepted ), Then the subsequent delegation will be processed normally , Otherwise, the transaction gateway will immediately retry with the first delegation , Until the door knocks .

The platform status is “ It's about to open up ” or “ to open up ” The counter system can make declaration , The delegation sent to the gateway in other states will be represented by “ The platform is not open ” Refuse .

The reason for knocking on the door is “ The platform is not open ” The service rejection of will be handled automatically by the gateway ( Continue to try again ), Not to the counter .

The counter can continue to report when knocking on the door , But delegates will be cached in the buffer of the gateway operating system , The gateway will not receive until it succeeds .

8、 Market gateway

The quotation gateway is used to provide quotation services . Different market information is divided into multiple channels , Market participants can choose to receive only the market information of the specified channel according to their needs .

Level2 The transaction by transaction entrustment and transaction by transaction of the market compose a data stream to send the real-time market release frequency 、 The number of Market Snapshot orders can be configured according to business needs .

9、 Transaction access network

The transaction access network of Shenzhen stock exchange is as follows :

(1) Business : transaction +Level I The market

Ø Wide area access : securities company (10M)、 Fund company (6M or 10M)

Ø Managed access :1G or 10G LAN

(2) High speed market network

Ø Business : Level II The market (Level I Quotes as backup )

Ø Wide area access :10M above

Ø Managed access :1G or 10G LAN

(3) High speed unidirectional satellite

Ø Business : Level I The market

Ø Alternate channels for transaction participants ; Active or standby for pure market users

(4) Bidirectional satellite

Ø Business : Backup channel for transaction business data

- service function

The trading hours of Shenzhen Stock Exchange are as follows :

The risk control and transaction management functions of SZSE are as follows :

11、 Match the engine

The core of the exchange trading system , Used to match sales and purchase orders . Since the matching engine needs to match the orders of all buyers and sellers in the securities market , Therefore, the stable operation of the matchmaking engine is very important to ensure the normal operation of the exchange .

The matchmaking engine is in the computer room of the exchange , In order to transfer orders to the exchange for matching faster ,HFT The company will try its best to keep its mainframe close to the data center of the exchange .

12、 Exchange machine room custody

Domestic exchanges have their own server hosting centers , Shanghai Securities Exchange trusteeship machine room, Waigaoqiao, Shanghai Stock Exchange 、 Shenzhen tongtuoguan machine room of South Center of Shenzhen Stock Exchange 、 Shanghai Stock Exchange Jinqiao trusteeship machine room . Only securities 、 A futures company may rent a custody machine room cabinet from the exchange . negotiable securities 、 Futures companies provide cabinets 、 Buy equipment 、 Purchase or rent software to serve its customers . High end procedural trading teams usually purchase equipment by themselves or specify hardware configuration by securities 、 Futures companies purchase , Securities 、 The futures company agrees , Put it into the rented cabinet for transaction .

Co-location Applicable to low delay transaction users .HFT The company or proprietary trading team can apply for cabinets and network resources from securities companies or futures companies , Place the trading host and the trading host of the exchange as close as possible in physical distance .

The custody machine room provided by the exchange is limited by the site and power , General resource capacity is limited , Supply often exceeds demand .

Four 、 Quantitative trading system architecture

1、 Introduction to the trading system

In the US electronic trading network , Investors can use the telephone 、 Traditional methods such as fax participate in transactions through brokers , It can also be directly connected through the trading market (DMA) Methods such as , Skip broker brokering , Directly participate in ECN And other electronic trading networks , Or choose more anonymous transaction execution through various securities cross networks . During the execution of the transaction , Order management system (Order Management Systems,OMS) And order execution management system (Execution Management System,EMS) It plays an important role in the whole trading network .

OMS( Order management system ) It is the center of trading activities of all buyer investors , Focus on providing investors with electronic trading capabilities , Used to allow investors to manage and record their electronic trading activities , Used by buyer investors to interact well with their brokers , Especially based on FIX(Financial Information Exchange) Transaction management system . With the development of trading technology ,Direct Market Access(DMA) The introduction of 、 Algorithmic transaction and order routing (Order Routing) Appearance , Buyer transactions urgently need a new 、 A system that focuses more on managing the transaction execution process than just the interaction and recording functions , The solution came later EMS( Order execution management system ).EMS Focus on strengthening brokers in the direct market (Direct Market)、 Algorithm trading and other aspects of the implementation of electronic trading strategies , That is, through the embedded algorithm trading engine , utilize ECN、Crossing Network, etc , Look for multiple trading options , So as to explore more comprehensive sources of liquidity .

With the development of the market , The execution management system and the order management system tend to be close to each other ,EMS and OMS It also gradually has some functions of the other party's system .

2、 Classification of trading system

at present EMS/OMS The system is classified as follows :

(1)OMS.

Most buy side organizations do not have a strong need for senior executive management capabilities , And the existing order management system has met the required functions , Therefore, some of the buyer's organizations are only in OMS Order management system .

(2)EMS

Some organizations choose EMS, Advanced executive management capabilities and speed are key determinants of the platform . Most hedge funds with active trading strategies use EMS.

3) be based on FIX Integration of EMS/OMS

Integrate EMS and OMS The platform of , Customers can be in EMS Manage all execution functions on , But rely on OMS To perform basic order management 、 Verification and settlement, etc .

4) Fully integrated EMS/OMS.

In the long run , A more stable transaction execution platform must be fully integrated EMS and OMS. However, due to the complexity of code layer integration and data flow coordination , Integration is not easy .

OMS(Order Management System) It is the core business system of order management , A typical case is the large centralized system of major securities companies .

EMS(Execution Management System) It is a core business system that provides more order types and order execution , yes OMS Strong help from .

PMS(Portfolio Management System) It is a system that provides portfolio analysis for customers , Provide information such as asset reports 、 Transaction report 、 Combinatorial analysis 、 Profit analysis 、 risk analysis 、 Transaction behavior analysis 、 Account diagnosis 、 Risk control, compliance and other functions .

POMS(Portfolio and Order Management System) yes PMS and OMS A general term for a combined system .

3、 Quantify the transaction structure

Excellent quantitative trading system has the fastest line to receive market data 、 The fastest data processing and reading ability 、 The best policy software 、 The fastest trading channel , Every link is indispensable .

4、 The practice of trading system in European and American stock markets

at present , Institutional investors in the European and American securities markets are mostly based on their own needs , Choose a transaction execution system that suits you . According to the transaction frequency and the complexity of the investment strategy, the right of the institution OMS And EMS The choices are well divided . Use more complex trading strategies , Such as statistical arbitrage 、 High frequency black box (Black Box) And other institutions with frequent transactions , Usually prefer to use EMS; Use only simple trading strategies , If only buy and hold 、 Institutions that pay attention to global macro, etc. and do not trade frequently , Usually only OMS that will do ; long-term investment , In particular, most pension funds 、 Mutual funds, etc , Preference OMS; Hedge funds , In particular, hedge funds that use advanced trading algorithms and Strategies , They tend to EMS.

5、 ... and 、 Transaction execution strategy

1、 Introduction to transaction execution

In securities investment activities , Transaction execution is the most basic behavior . Whether portfolio trading or complex arbitrage strategy , Ultimately, it will be realized by basic buying or selling . With the increasing scale of asset management , The trading behavior of institutional investors has a greater and greater impact on the market . How to buy or sell large securities without disturbing the market, so as to bear lower transaction costs and avoid abnormal market fluctuations , It has become one of the most concerned issues of institutional investors and securities regulatory authorities .

Algorithmic Trading (Algorithmic Trading) Provides a solution . Algorithmic trading technology transforms the target of transaction execution into a specific strategic model in the form of Financial Mathematics , Based on computer technology and information technology, the instruction flow of securities orders is computerized ( Procedural 、 Algorithmic ) And execute the transaction in an appropriate mode , In order to obtain high execution quality .

In mature markets , Users of algorithmic trading include brokers 、 Hedge funds 、 Pension funds 、 Mutual funds and proprietary trading departments with their own algorithmic trading systems .

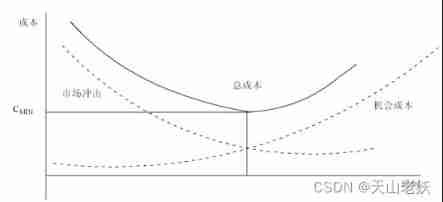

2、 Transaction costs

Transaction costs in securities investment activities can be divided into exogenous costs and endogenous costs . Exogenous costs include commissions 、 Stamp duty, etc , The exchange and the regulatory authorities set the charge rate , Generally, the size of the stock can be determined before the actual trading ; Endogenous cost refers to the influence of market conditions in the process of stock transaction 、 The cost caused by the impact of implementation and other factors , Also known as transaction execution costs , It includes opportunity cost and impact cost . Impact cost refers to the impact of order transaction on market price . When the order size is equal to or less than the optimal quotation level ( That is, the best selling gear or the best buying gear ) The depth of the market , The order can be executed at the best buy or sell price ; When the order size exceeds the optimal quotation level ( That is, the best selling gear or the best buying gear ) The depth of the market , The trading of orders will cause the market price to change in a direction unfavorable to traders . therefore , The larger the transaction volume of the order, the greater the impact cost . Opportunity cost refers to the period from the time the investor places an order to the time the order is executed ( Or cancel the order without execution ) Price risk over time . As new information enters 、 Investor sentiment 、 Temporary lack of liquidity and other factors , The fluctuation of securities price will lead to a certain difference between the order execution price and the order release price , This is the opportunity cost of the order .

The collection of exogenous costs is mostly subject to a fixed service fee system , The exogenous costs that investors need for each transaction are very clear ; The transaction uncertainty caused by the uncertainty of market conditions and the endogenous nature of execution makes the transaction execution cost implicit , It often leads many investors to regard the exogenous cost as the total transaction cost and ignore the existence of transaction execution cost .

according to ITG Announced trading execution losses (IS) Method to measure the transaction execution cost of major securities markets , stay 2012 Second quarter , The endogenous costs in the world's major markets account for... Of the total transaction costs 84%, And the external generated cost only accounts for 16%, It shows the importance of transaction execution cost composed of opportunity cost and impact cost in the total cost in the trading process of overseas mature securities markets .

3、 Basic framework of transaction execution strategy

Investors need to weigh whether to choose immediate trading or deferred trading , Ensure that appropriate execution strategies are selected to minimize transaction costs . Demand for large transactions , When formulating the execution strategy, it is necessary to discuss in depth how long the execution should be completed , How big a position to execute each time .

Investors can complete large transactions through one-time transactions or split orders . When selecting the former , Large transactions are likely to have a greater impact on the market , As a result, the actual transaction price changes in an unfavorable direction , Institutional investors need to bear higher market shock costs ; When choosing the latter , Although it can effectively reduce the impact on the market , However, it often takes a long time for a large transaction to be completed , Institutional investors must bear the risk of large price fluctuations , That is, bear higher opportunity cost . So , Institutional investors must make a trade-off between the market shock cost and opportunity cost caused by different execution strategies , Choose to match your risk appetite 、 The most effective execution strategy , That is, what kind of transaction strategy to adopt and how to determine the scale of split orders .

Suppose that an institutional investor is considering (0,T) The size of the positions bought or sold between X Shares ( Can be bought or sold , Take selling for example ). The position size of institutional investors at the initial time is X,T The remaining position at the moment is 0. Let the trading position at each time point be xi, The sequence represents a transaction execution strategy . In the course of the actual transaction , There are countless different transaction execution strategies , Take abscissa as time , The ordinate is the coordinate system of the size of the position held to represent the whole execution process . Suppose you can't buy in the process of selling , Then each execution process can be represented as a connection (0,X) Point and (T,0) The descent trajectory curve of a point .

Investors face different risk and return choices under different execution strategies , Investors with different risk preferences will choose different execution strategies . For risk neutral investors , Only the execution cost in the transaction process is concerned , Regardless of the risks in the implementation process , Trading may be more inclined to extend the trading time , Split the order into smaller parts , To avoid price shock to the market , It may choose a uniform execution strategy C; Risk averse investors are reluctant to take even the smallest price risk , It will choose the execution strategy A, Sell all at the beginning of the transaction , Minimize uncertainty ; For investors who are extremely risk averse , The execution strategy will be selected E. For other risk averse investors , Investors will be based on their own risk appetite , Choose the right execution strategy for yourself .

4、 Method of transaction execution strategy

The proper choice of execution strategy is the core and key to the success of investors in trading . In electronic trading , The choice of execution strategy is more reflected in the choice and use of algorithm trading strategy . Specific performance: , Investors use computer algorithms to decide when to place orders 、 The price and even the quantity and quantity of the final order , By decomposing a large transaction into several small transactions , In order to better manage the market shock costs 、 Opportunity costs and risks . With the development of trading technology and the in-depth study of execution strategy theory , The algorithm of transaction execution is also developing :

A. First generation algorithmic trading strategy

The problem to be solved in the original algorithmic trading is that computers can replace manual orders , To achieve the purpose of issuing trading orders according to a certain mode at regular intervals , It mainly realizes the function of order submission . For example, the volume weighted average price that is most used in the international market (VWAP)、 Time weighted average price (TWAP).

B. Second generation algorithmic trading strategy

The second generation of algorithmic trading strategy on trading execution begins with the qualitative change of investors' understanding of the optimal execution strategy . The second generation algorithmic trading strategy has begun to pay attention to the following issues : During a certain transaction execution period , How to allocate the execution position at each time point to minimize the transaction cost ? If similar VWAP Or an average strategy that trades at every moment , How to determine the execution period of the transaction , It was a day , It's still a week , How to choose trade-offs in execution speed ? On the whole , This kind of algorithm will not actively select the trading time and quantity according to the market conditions , Instead, they trade for a given purpose , So it is also called passive algorithmic trading , Or structured algorithmic trading . Such as using more arrival prices in the international market (Arrive Price) Strategy 、 Execution loss (Implementation Shortfall) Algorithm .

C. Third generation algorithmic trading strategy

The second generation algorithmic trading strategy believes that the market is stable and predictable , Once the execution strategy is obtained from the model and data , Regardless of changes in liquidity and other market conditions , Transactions generally do not deviate from the intended trajectory . But in reality , Models based on historical data cannot take into account some extreme market conditions , This makes investors expect that when market conditions change , The transaction execution strategy can be adjusted adaptively . therefore , In industry practice, there are many proactive strategies that change the urgency of implementation with the price movement . In addition to considering how to reduce the execution cost and price risk that the second generation algorithm trading strategy focuses on , This kind of adaptive trading algorithm turns its focus to price trend prediction . for example , If investors judge that the market price is moving in a favorable direction, they will delay the transaction , On the contrary, it will speed up the transaction ; When there is a strong mean reversion phenomenon in the market price , Investors are able to catch a favorable offset .

at present , The most common algorithmic trading strategies include VWAP、TWAP、Target Volume、Arrive Price, It is available in most brokers' systems . Besides , There are also strategies that institutions have tailored to their customers . for example , stealth ( Stealth )、 Guerrilla detachment 、 The sniper (Sniper)、 Sniffer (Sniffer) etc. . For the existing algorithmic trading system of overseas institutional investors , Some institutional investors' algorithmic trading systems need to provide user-defined parameters . for example , The number of trades that need to be customized 、 The way of execution 、 Selected algorithm trading strategy 、 Trading start and end time 、 Proportion of transaction volume involved, etc , The setting of these parameters determines the execution of the transaction by the trading system , such as Instinet Of Execution Experts Yes VWAP Policy setting ( See the picture 3). Again , Some institutional investors can fully embed the optimal transaction execution strategy developed by themselves into the trading system , For example, famous overseas transaction execution service providers ITG company ACE The optimal execution strategy of the system .

With the further research and improvement of execution strategy , Algorithmic trading strategies have been adopted by hedge funds 、 Pension funds 、 Mutual funds and other institutional traders are widely used , Major brokers or third-party trading service providers have developed management systems embedded in algorithmic trading , It has been applied in most brokers or third-party transaction execution service providers in the United States , Such as Bank of America Electronic Algorithmic Strategy Execution (EASE), Barclays Capital LME System , Credit Suisse Advanced Execution Services, Morgan Stanley Benchmark Execution Strategies (BXS) etc. . According to the service provider's classification of customers using these systems , At a securities broker (Broker/Dealers)、 Hedge funds (Hedge Funds)、 Mutual funds (Mutual Funds)、 Proprietary trading department (Proprietary trading desks) Among the four types of customers , Most of them are hedge funds and mutual funds , In the vast majority of service providers, more than half of customers come from these two categories . With the expansion of algorithmic trading service providers, large-scale investment banks 、 Brokers spend a lot of money on research every year , It is used to develop algorithms that can more quickly meet customers' personalized needs , To open the gap with competitors in the same industry . And those small institutions can hardly afford the huge R & D expenses , Have to buy algorithms from large institutions .

5、A Stock market trading execution strategy practice

The transaction is executed at A The stock market is still in its infancy , In practice , There are few applications for transaction execution , The program is relatively simple , The risk is basically controllable .A The trading execution characteristics of the stock market are as follows :

(1) Mainly in manual order mode , Transaction execution is supplemented by placing orders , However, the proportion of orders placed by transaction execution is increasing .

since 2009 Since then , Trading execution is gradually introduced into the domestic securities market , It has been valued by market participants .

In terms of funds , By 2012 end of the year , Domestic fund companies have a total of 73 home , Most of the counter systems are Hang Seng 03 System . at present , The system has been embedded in the algorithm trading modules of UBS Securities and Guosen Securities , Including China 、 Jiashi 、 E Fonda 、 Boshi 、 South, etc 20 Fund companies have purchased the transaction execution technology system , And use transaction execution in actual transactions . Some management scale is large 、 The proportion of fund companies with large trading volume using transaction execution to conduct transactions continues to increase . for example , Huaxia 、 Jiashi 、 The stock trading volume of ICBC Credit Suisse and other companies is about 15% to 25% Completed by transaction execution . The conclusion of our previous analysis on the execution cost of fund transactions further indicates that the proportion of transaction execution is gradually increasing .

In the securities business , UBS Securities 、 Guosen securities 、 Haitong securities 、 Citic securities, 、 GF Securities and others have started to develop transaction execution strategies . stay 2009 year 7 month , UBS Securities uses trading execution in QFII In terms of business, carry out agency client brokerage business , Trading execution was officially launched at UBS Securities , At present, the trading volume of UBS Securities has accounted for... Of the total trading volume 80%. The transaction execution service of Guosen Securities is in 2010 Officially launched in Bloomberg system in , Become the first local securities firm to launch the A Stock market algorithmic trading service securities companies , Global institutional investors can choose to use Guosen Securities algorithmic trading service to participate in investment and trading in China's securities market through Bloomberg terminals spread across major financial institutions . CITIC Securities is in 2012 Annual choice Progress software company Apama Algorithm trading platform , Provide institutional investment clients with low delay and high frequency algorithm trading strategies including transaction execution . GF Securities is in 2012 In, he chose the United States StreamBase and Thomson Reuters Cooperate to provide an algorithm platform to develop transaction execution strategies .

(2) The technical procedures for transaction execution are simple , Application objects are limited

Take the fund industry as an example , At present, the fund company adopts a relatively simple and mature transaction execution model in the overseas market , Such as volume weighted average price (VWAP)、 Time weighted average price (TWVP) etc. , For others, such as execution differences (IS) And other improved algorithms are rarely used . In terms of application objects , At present, transaction execution is mainly applied to large circulating market value 、 Stocks with good liquidity and less volatility . As the transaction execution technology has not been applied in China for a long time , The concrete effect needs to be tested , For small and medium cap stocks with high volatility , The fund is still dominated by manual orders .

(3) Transaction execution advantages appear , But it is not yet fully revealed

Although domestic transaction execution advantages have emerged , But it is not yet fully revealed . The reason lies in , The lack of some transaction systems in China limits the development of transaction execution , This further hinders the full demonstration of the advantages of transaction execution . To be specific , The limitations of transaction execution in China include :

A. T+1 Trading system . China's stock market currently adopts T+1 Trading system , Algorithmic trading generally requires a large number of intra day transactions .T+1 Trading mechanism will undoubtedly bring great obstacles to algorithmic traders who mainly deal in high-frequency transactions .

B. High transaction costs . The transaction cost of China's stock market is higher than that of other countries or regions , In particular, there is a unilateral transaction amount in stock trading 0.1% Stamp duty on , It has a greater impact on algorithmic trading .

C. Data has a high latency problem . There is a problem of data delay in China's stock market , This will restrict the smooth progress of algorithm trading . at present , The market information in the stock index futures market is revealed in real time , However, the general situation in China's stock market is revealed as 5 second / Time ,Level2 The speed of market disclosure is only 3 second / Time . therefore , At present, there is a high delay in stock market data , This is not conducive to professional investors to carry out algorithmic trading .

If the above problems are solved , With the complexity of transaction technology and the increase of transaction frequency , The advantages of transaction execution will be further revealed , Institutional investors will pay more attention to transaction execution , And put more effort into the implementation of this technology

6、 ... and 、 Transaction execution process

1、 Introduction to transaction execution process

The trading system network is only the hardware guarantee for investors to execute transactions , Investors are equally important for Software Assurance such as application means and strategy selection in the transaction execution process . In the mature securities markets in Europe and America , Investors' transaction execution process is usually divided into pre transaction planning (Pre-Trade Strategy Plan)、 Transaction execution process monitoring 、 Post transaction analysis .

2、 Pre deal planning

After deciding on the specific tasks of the transaction , Investors need to make the following analysis on transaction execution :

(1) Transaction execution subject matter analysis (Identifying Potential Outliers)

The investor first analyzes the execution target of the portfolio transaction , Fully obtain the historical execution characteristics of the execution object , To identify potential targets that need special consideration . for example , It is necessary to identify those with poor liquidity 、 Securities that are difficult to trade 、 Transactions with large execution costs or accounting for a large proportion of the average daily trading volume .

(2) Selection of liquidity sources and trading methods

After identifying the execution profile of the transaction object , Investors need to analyze the source of liquidity of the underlying securities , To select the appropriate execution system, etc . With ITG For example , For highly liquid stocks , have access to ITG Volume based strategies Horizon smart server; For stocks with poor liquidity or transactions with a large proportion of positions relative to the average daily trading volume , You can manually find the liquidity pool (Liquidity Pools) Or through the matching system of block trading (Block-Matching System), namely ITG Of POSIT etc. .

(3) Choice of execution strategy

Execution strategies are represented by various algorithmic trading strategies in industry practice , That is to say, the large amount transaction is decomposed into several small amount transactions according to the set form , In order to better manage the market shock costs 、 Opportunity costs and risks . Different institutions in the market have developed a large number of different forms of algorithmic trading , Various algorithmic transactions have their own characteristics , The choice of algorithmic trading focuses on the needs of investors , There is no optimal algorithmic trading strategy in any case .

Different investors have different trading styles and risk preferences , The characteristics of investors will affect the choice of execution strategy . Some investors may be desperate to trade , Most of the execution in the transaction will be completed in the morning , Other investors may be very patient , Choose to execute slowly over a longer period of time ; Different investors have different transaction cost benchmarks , For example, an index fund may want to buy at a price as close to the closing price as possible . Besides , In the process of trading , If the stock price or trading volume changes , Investors' willingness to invest may also change , These are the factors that affect the choice of algorithmic trading . therefore , Choose the right strategy to execute various transactions , We need to learn from the characteristics of the stock 、 Market conditions 、 Investors' risk preference, etc , Compare the performance of various strategies based on historical parameters , Execute by selecting the best matching policy .

3、 transaction Execution process monitoring

After the transaction begins , Unexpected events or information may occur , So as to change the setting of transaction execution , Affect the performance of transaction execution . If the various factors that make up the implementation of the strategy change , Investors need to change their execution strategies to cope with sudden changes . for example , Strategies based on trading volume distribution are very sensitive to information or events that affect trading volume distribution , When the market publishes information that may lead to significant changes in trading volume during the execution of the transaction , If investors do not change their execution strategies in time , It may make the trading strategy face disastrous results .

therefore , Investors need a monitoring system to evaluate the possibility of an emergency and the impact of the event on the implementation of the strategy . Simple trading volume signals and real-time optimal bid ask spreads can help investors better deal with information events in the process of implementing strategies .

4、 Post transaction analysis

After the transaction is executed , Investors need to evaluate the execution quality of the transaction , That is to identify and analyze the difference between the estimated implementation cost and the actual implementation cost of the predetermined target . The analysis of price difference can help investors understand the reasons for the change of execution cost —— It is the drastic change of market conditions , Or the improper choice of execution strategy . for example , If you use VWAP Strategies to trade illiquid stocks , There may be a large price difference , Because the trading volume model of low liquidity stocks is difficult to accurately predict , It will affect VWAP The quality of policy execution , Post transaction analysis usually identifies unreasonable price differences . Post transaction analysis is very important for feedback on transaction execution , The analysis conclusion obtained from it will affect the choice of future transaction execution .

边栏推荐

- Work assessment of pharmaceutical polymer materials of Jilin University in March of the 22nd spring -00025

- AI writes its own code to let agents evolve! The big model of openai has the flavor of "human thought"

- Void* pointer

- How far is the memory computing integrated chip from popularization? Listen to what practitioners say | collision school x post friction intelligence

- Randla net: efficient semantic segmentation of large scale point clouds

- Interview with Mo Tianlun | ivorysql wangzhibin - ivorysql, an Oracle compatible open source database based on PostgreSQL

- 可能是拿反了的原因

- 论一个优秀红队人员的自我修养

- The art of writing simple code

- Dr. Sun Jian was commemorated at the CVPR conference. The best student thesis was awarded to Tongji Ali. Lifeifei won the huangxutao Memorial Award

猜你喜欢

Redis related-03

![[rust submission] review impl trail and dyn trail in rust](/img/bc/05b3e031659ce19d6f6e3887d70512.jpg)

[rust submission] review impl trail and dyn trail in rust

Background page production 01 production of IVX low code sign in system

吴恩达机器学习新课程又来了!旁听免费,小白友好

Musk: Twitter should learn from wechat and make 1billion people "live on it" into a super app

Now, the ear is going into the metauniverse

How far is the memory computing integrated chip from popularization? Listen to what practitioners say | collision school x post friction intelligence

Crawler grabs the data of Douban group

完美洗牌问题

Tencent Open Source Project "Yinglong" est devenu un projet Apache de haut niveau: l'ancien Service à long terme Wechat payment, peut maintenir un million de milliards de niveaux de traitement de flux

随机推荐

Maybe it's the wrong reason

Tensorflow, danger! Google itself is the one who abandoned it

JSP cannot be resolved to a type error reporting solution

俄罗斯AIRI研究院等 | SEMA:利用深度迁移学习进行抗原B细胞构象表征预测

OpenSUSE installation pit log

太极图形60行代码实现经典论文,0.7秒搞定泊松盘采样,比Numpy实现快100倍

Maintenant, les oreilles vont entrer dans le métacosme.

Create SQLite table with shell script and add SQL statement -- General

BGP biplane architecture

Work assessment of Biopharmaceutics of Jilin University in March of the 22nd spring -00005

【Rust投稿】捋捋 Rust 中的 impl Trait 和 dyn Trait

[rust submission] review impl trail and dyn trail in rust

Jilin University 22 spring March "official document writing" assignment assessment-00084

Do you really need automated testing?

Disassembly of Weima prospectus: the electric competition has ended and the intelligent qualifying has just begun

Crawler grabs the data of Douban group

Wuenda, the new course of machine learning is coming again! Free auditing, Xiaobai friendly

Sun Wu plays Warcraft? There is a picture and a truth

Two common OEE monitoring methods for equipment utilization

Huawei failed to appeal and was prohibited from selling 5g equipment in Sweden; Apple regained the first place in the world in terms of market value; DeNO completes round a financing of USD 21million