当前位置:网站首页>Mathematical modeling - linear programming

Mathematical modeling - linear programming

2022-06-25 17:16:00 【Herding cattle】

Catalog

Basic concepts

An important branch of operations research is mathematical programming , Linear programming is an important branch of mathematical programming .

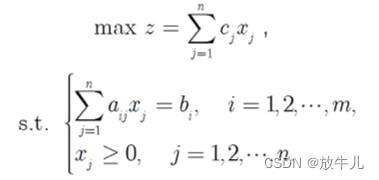

Variables are called The decision variables , The goal of the plan is called Objective function , The restriction is called constraint condition ,s.t. yes “ Bound ” It means .

The general steps of establishing a linear programming model are :① To analyze problems , Find out the decision variables .② Find equality or inequality constraints .③ Construct a linear function about decision variables .

General form of linear programming model :

or :

![c=[c_{1},c_{2},...,c_{n}]^{T}](http://img.inotgo.com/imagesLocal/202206/25/202206251650024986_1.gif) Is the coefficient vector of the objective function , Also called value vector ;

Is the coefficient vector of the objective function , Also called value vector ;![x=[x_{1},x_{2},...,x_{n}]^{T}](http://img.inotgo.com/imagesLocal/202206/25/202206251650024784_12.gif) Is the decision vector ;

Is the decision vector ; Is the coefficient matrix of the constrained equations ;

Is the coefficient matrix of the constrained equations ;![b=[b_{1},b_{2},...,b_{m}]^{T}](http://img.inotgo.com/imagesLocal/202206/25/202206251650024986_9.gif) Is the constant vector of the constrained equations .

Is the constant vector of the constrained equations .

And standard :

The objective function is very large , The constraints are equality constraints . The solution satisfying the constraint conditions is a feasible solution , Making the objective function reach the maximum value is called the optimal solution . The set of all feasible solutions is called feasible region , Write it down as R.

In the process of solving mathematical programming problems , Be sure to calculate Sensitivity analysis . Sensitivity analysis refers to the analysis of the sensitivity of the system due to changes in surrounding conditions . For linear programming problems a、b、c Are set to constant , But in practice , These coefficients will change a little .

Model solving and application

MATLAB There are two models for solving mathematical programming problems in : Solver based solution method and Problem based solution ,

Solver based solution method

It is necessary to convert linear programming into standard form :

The objective function must be minimized , Constraints are divided into less than or equal to constraints and equal sign constraints ,lb and ub Is the upper and lower bounds of decision variables .

MATLAB The function call format is :

[x,fval] = linprog(f,A,b)

[x,fval] = linprog(f,A,b,Aeq,beq)

[x,fval] = linprog(f,A,b,Aeq,beq,lb,ub)

x Returns the value of the decision variable ,fval It returns the optimal value of the objective function ,f It's the value vector ,A,b Corresponding to the linear inequality constraint ,Aeq and beq Corresponding to the constraints of linear equality ,lb and ub Corresponding to the lower bound vector and the upper bound vector of the decision vector respectively .

This method can only be applied to The decision vector is one-dimensional The situation of .

Problem based solution

First, the optimization problem is constructed with variables and expressions , And then use solve Function solving , It can be used doc optimproblem view help .

①prob=optimproblem('ObjectiveSense','max');

ObjectiveSense It can be max and min, Represents the maximum or minimum value of optimization , The default is min

② Definition f,A,b( ditto ,f Can be defined as a row vector , In this way, the objective function is different and then transposed )

③x=optimvar('x',2,1,'TYPE','integer','LowerBound',0,'UpperBound',inf);

first ‘x’ Inside is the variable name , Column vector , Then there are several rows and columns .

‘TYPE’, What is defined later is the type of the function , for instance integer Integer type ,double Double precision models

‘LowerBound' And 'UpperBound' Indicates what the lower and upper bounds follow 0,inf They are the scope

④prob.Objective=f * x;% Objective function , The objective function needs to get a scalar value , Not a matrix vector

⑤prob.Constraints.con=A*x<=b;% constraint condition , There is only one constraint , Or you can skip it .con,.con Is the label , You can name it yourself , When there are multiple constraints , Must label cannot be the same .

⑥[sol fval flag out]=solve(prob);%fval It's the best value ,sol.x Is the value of the decision variable , When there are multiple decision variables , Sure sol.y,flag Don't worry about in linear programming , Note that it cannot be negative in nonlinear programming .

for example :

Use solver to solve :

clc,clear

f = [-2;-3;5];% To find the minimum

A = [-2,5,-1;1,3,1];

b = [-10;12];

Aeq = [1,1,1];

beq = [7];

lb = zeros(3,1);

[x,fval] = linprog(f,A,b,Aeq,beq,lb,[]);

x

-fvalx =

6.4286

0.5714

0

ans =14.5714

Use problem-based solutions

clc,clear

prob=optimproblem('ObjectiveSense','max');

x=optimvar('x',3,'LowerBound',0);

prob.Objective=2*x(1) + 3*x(2) - 5*x(3);

prob.Constraints.con1=2*x(1) - 5*x(2) + x(3)>=10;

prob.Constraints.con2=x(1) + 3*x(2) + x(3)<=12;

prob.Constraints.con3=x(1) + x(2) + x(3)==7;

[sol fval flag out]=solve(prob);

sol.x

fvalans =

6.4286

0.5714

0

fval =14.5714

other

- MATLAB in , Load existing txt Matrix of documents , If use load function , Then the number of rows and columns of the matrix should be equal . If individual numbers are missing , You can use readmatrix function .writematrix(a,'data.xlsx') Can write Excel in .

- Matrix index a(1:end,1),end It is automatically the last column of the row

- sum(a,'all') According to matrix a The sum of all the elements of

边栏推荐

- 卡尔曼时间序列预测

- SMART PLC如何构造ALT指令

- Using pywebio testing, novice testers can also make their own testing tools

- Singleton mode application

- 2022-06-17 advanced network engineering (IX) is-is- principle, NSAP, net, area division, network type, and overhead value

- Why are there few embedded system designers in the soft test?

- 学习太极创客 — MQTT(三)连接MQTT服务端

- Wireshark network card cannot be found or does not display the problem

- TCP聊天+传输文件服务器服务器套接字v2.8 - 修复已知程序4个问题

- 2022-06-17 advanced network engineering (x) is-is-general header, establishment of adjacency relationship, IIH message, DIS and pseudo node

猜你喜欢

Which is better for intermediate and advanced soft exam?

How did I raise my salary to 20k in three years?

项目经理在项目中起到的作用

内卷?泡沫?变革?十个问题直击“元宇宙”核心困惑丨《问Ta-王雷元宇宙时间》精华实录...

学习太极创客 — MQTT(一)MQTT 是什么

知道这些面试技巧,让你的测试求职少走弯路

SDN系统方法 | 10. SDN的未来

Wechat official account server configuration

这些老系统代码,是猪写的么?

What are the steps for launching the mobile ERP system? It's important to keep it tight

随机推荐

宝藏又小众的国画3d材质贴图素材网站分享

How does social e-commerce operate and promote?

How to talk about salary correctly in software testing interview

Which is better for intermediate and advanced soft exam?

Sword finger offer 50 First character that appears only once

try with resource

内卷?泡沫?变革?十个问题直击“元宇宙”核心困惑丨《问Ta-王雷元宇宙时间》精华实录...

The role of the project manager in the project

万卷书 - 大力娃的书单

Wechat official account server configuration

TCP聊天+传输文件服务器服务器套接字v2.8 - 修复已知程序4个问题

XXIX - orbslam2 real-time 3D reconstruction using realsensed435

Kotlin

Structure de la mémoire JVM

微信公众号服务器配置

Ten thousand volumes - list of Dali wa

Pytorch official document learning record

Wireshark network card cannot be found or does not display the problem

Redis series - overview day1-1

Redis系列——概述day1-1