当前位置:网站首页>Time series analysis - how to use unit root test (ADF) correctly?

Time series analysis - how to use unit root test (ADF) correctly?

2022-06-25 12:06:00 【Halosec_ Wei】

1、 effect

When using many time series models , Such as ARMA、ARIMA, Will require the time series to be stable , So when studying a time series , The first step is to test the stability , In addition to the method of visual inspection , In addition, the more commonly used strict statistical test method is ADF test , Also called unit root test . Unit root test refers to checking whether there is a unit root in the sequence , Because there is a unit root, it is a nonstationary time series .

2、 Input / output description

Input :1 Quantitative variables of time series data

Output : The sequence data is stable in several order difference

3、 Learning Websites

SPSSPRO- Free professional online data analysis platform

4、 Case example

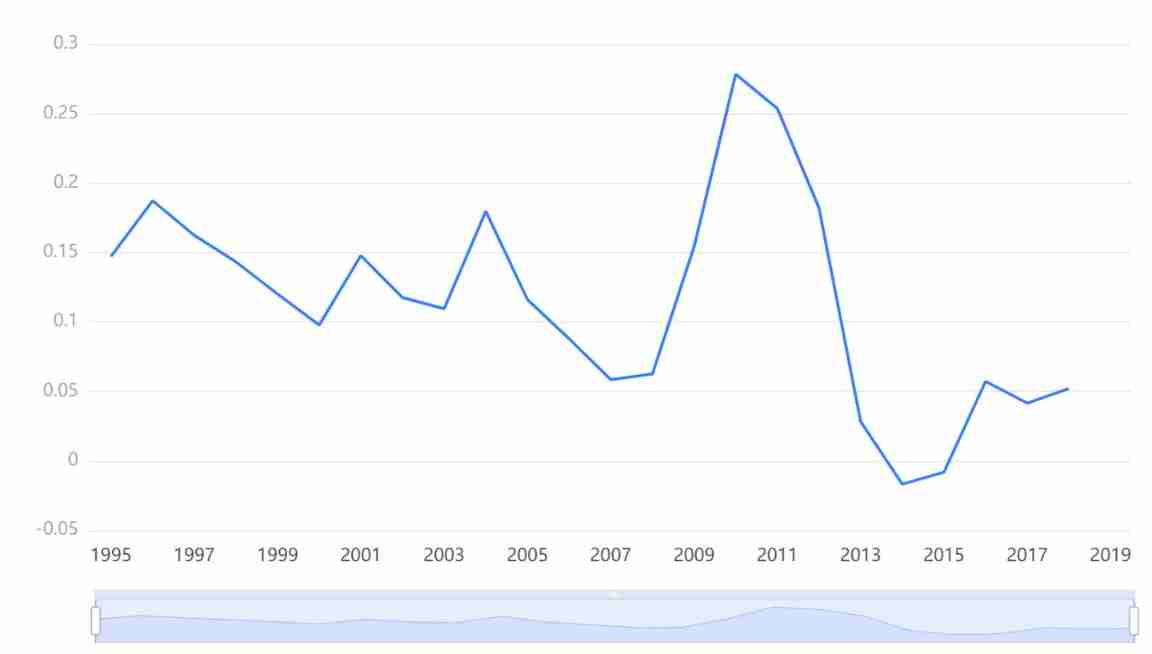

Case study : Based on a magazine 1995-2019 Annual printing volume data , Judge whether it is stable .

5、 Case data

Unit root test (ADF) Case data

6、 Case operation

Step1: New analysis ;

Step2: Upload data ;

Step3: Select the corresponding data to open and preview , Click start analysis after confirmation ;

step4: choice 【 Unit root test (ADF)】;

step5: View the corresponding data format ,【 Unit root test (ADF)】 Request input 1 Quantitative variables of time series data .

step6: Click on 【 To analyze 】, Complete the operation .

7、 Output result analysis

Output results 1:ADF Check list

*p<0.05,**p<0.01,***p<0.001

Chart description : The above table is ADF The results of the test , The results of this sequence test show that , Based on field print quantity ( ten thousand ): The difference is 1 Step time , Significance P The value is 0.000***, The level is significant , Rejection of null hypothesis , This series is a stationary time series . And in the original sequence and the difference is 2 Step time , Significance P Greater than 0.05, The original hypothesis cannot be rejected , Explain the original sequence and the difference 2 The order sequence is nonstationary .

Output results 2: Original sequence diagram

Chart description : The figure above shows the original figure without difference . among X The axis represents the time item ( year ),Y The axis represents the value ( Magazine print volume ), Subjectively , The original sequence diagram has an increasing trend , Is a nonstationary sequence .ADF The unit root test also shows that the first-order difference sequence is non-stationary .

Output results 3: First order difference graph

Chart description : The figure above shows the result of the first-order difference . When the time intervals are equal , Use the next value , Subtract the previous value , Get the first-order difference . Subjectively , The first-order difference sequence is numerically 1.5 Up and down , There is no obvious increasing and decreasing trend , It is preliminarily judged that the first-order difference sequence is a stationary sequence .ADF The unit root test also shows that the first-order difference sequence is stationary .

Output results 4: Second order difference graph

Chart description : The figure above shows the result of the second-order difference . Do the same action twice , That is, on the basis of the first-order difference, the latter value is subtracted by another value , Call “ Second order difference ”. For the stationary test of the second order difference sequence , adopt ADF The unit root test is used to obtain the non-stationary second-order difference sequence .

8、 matters needing attention

- Enter the time item of the page [ The nominal ] Variables are only rendered for drawing X For axis coordinates , No other meaning .

9、 Model theory

To any one AR(p) The process

![]()

His characteristic equation is :

![]()

If all the characteristic roots of the equation lie in the unit circle of , namely

![]()

Then the sequence is stable .

If there is a unit root , Then the sequence is nonstationary , And the sum of the regression coefficients is exactly equal to 1

![]()

10、 reference

[1] Wang Yan . Using time series analysis [M]. Beijing : Renmin University Press of China 2005.

边栏推荐

- 使用php脚本查看已开启的扩展

- Dark horse shopping mall ---6 Brand, specification statistics, condition filtering, paging sorting, highlighting

- Le détour d'un ingénieur en matériel

- plt.gca()画框及打标签

- Use of JSP sessionscope domain

- Recommend a virtual machine software available for M1 computer

- Flink deeply understands the graph generation process (source code interpretation)

- What are redis avalanche, penetration and breakdown?

- Sword finger offer II 091 Painting house: application of state machine DP

- plt. GCA () picture frame and label

猜你喜欢

优品购电商3.0微服务商城项目实战小结

Detailed explanation of Flink checkpoint specific operation process and summary of error reporting and debugging methods

云原生数据湖以存储、计算、数据管理等能力通过信通院评测认证

What are redis avalanche, penetration and breakdown?

一套自动化无纸办公系统(OA+审批流)源码:带数据字典

一款好用的印章设计工具 --(可转为ofd文件)

Why can't the form be closed? The magic of revealing VFP object references

Data Lake survey

19、wpf之事件转命令实现MVVM架构

黑马畅购商城---2.分布式文件存储FastDFS

随机推荐

Is it safe to open an account and buy stocks? Who knows

cnds

文献之有效阅读

依概率收敛

Problems encountered using easyexcel

Le détour d'un ingénieur en matériel

R语言dplyr包filter函数过滤dataframe数据中指定数据列的内容不是(不等于指定向量中的其中一个)指定列表中的数据行

How to open an account for trading futures Shanghai nickel products online

Tool usage summary

ROS notes (06) - definition and use of topic messages

Dark horse shopping mall ---2 Distributed file storage fastdfs

How do super rookies get started with data analysis?

做自媒体视频需要怎么做才能年收入一百万?

剑指 Offer II 091. 粉刷房子 : 状态机 DP 运用题

【OceanBase】OceanBase简介及其与MySQL的比较

黑马畅购商城---6.品牌、规格统计、条件筛选、分页排序、高亮显示

图片打标签之获取图片在ImageView中的坐标

优品购电商3.0微服务商城项目实战小结

SQL server saves binary fields to disk file

Sword finger offer II 091 Painting house: application of state machine DP