当前位置:网站首页>Information System Project Manager - Chapter VII project cost management

Information System Project Manager - Chapter VII project cost management

2022-06-27 06:06:00 【lufei0920】

Information system project manager — Chapter vii. Project cost management

The process of project cost management

Through project cost management, try to control the actual cost of the project within the budget range . Ensure that projects are completed within a comparable budget .

One 、 Planning cost management

Planning cost management : The project cost structure has been formulated 、 Estimate 、 Standards of budget and control .

1、 Type of cost

• Variable cost : With production 、 The cost that varies with workload or time is variable cost . Variable cost is also called variable cost .

• fixed cost : Not with production 、 Non recurring costs that change due to changes in workload or time are fixed costs .

• Direct cost : The cost directly attributable to the project work is the direct cost . Such as project team travel expenses 、 Wages 、 Fees for materials and equipment used in the project .

• Indirect costs : Expenses allocated to the project from the general management expense account or the project cost shared by several projects , It forms the indirect cost of the project , Such as tax 、 Additional benefits and security costs, etc .

• Opportunity cost : Is the use of a certain time or resources to produce a commodity , The lost opportunity to use these resources to produce other best alternatives is the opportunity cost , It generally refers to one of the biggest losses after making a choice .

• Sunk cost : It refers to what has happened due to past decisions , And costs that cannot be changed by any decision now or in the future . Sunk cost is a kind of historical cost , It's an uncontrollable cost to an existing decision , Will greatly affect people's behavior and decision-making , The interference of sunk cost should be eliminated in investment decision-making .

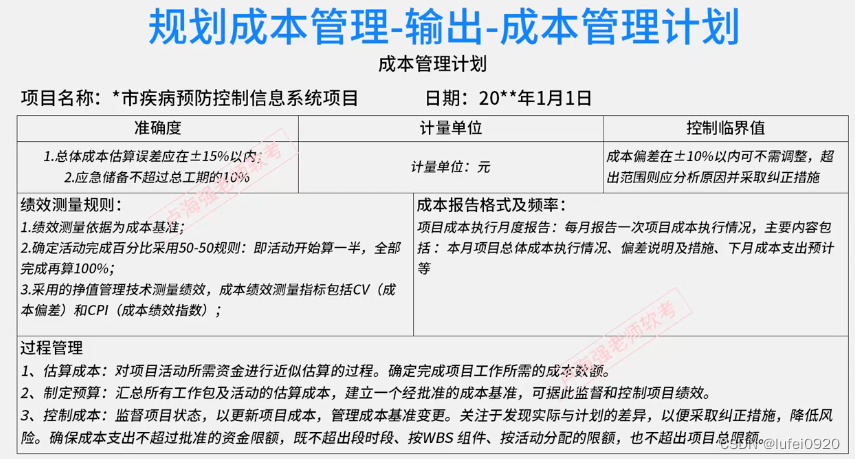

2、 Example cost management plan

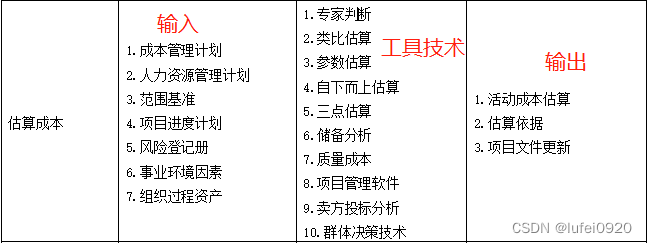

Two 、 Estimated cost

cost estimation : The process of preparing an approximate estimate of the funds required to complete the project activities .

1、 There are three main steps in project cost estimation

1) Identify and analyze component accounts of project cost , That is, the category of resources or services included in the project cost , for example : Labor cost 、 Material cost 、 Consulting fee, etc .

2) Accounts are formed according to the identified project cost , Estimate the cost size of each cost account .

3) Analyze the cost estimation results , Find various alternative costs , Coordinate the proportional relationship between various costs .

2、 Tool technology for cost estimation

2.1 Analogical estimation

Analogy estimation method is also called “ Top down estimation ”.

The basic operation steps of this method are :

First , The upper management personnel collect historical information about similar projects ;

secondly , Work with relevant cost experts to estimate the total cost of the current project ;

Again , Transfer the estimation results to the adjacent next level management personnel according to the hierarchy of the project work breakdown structure diagram , On this basis , They estimate the cost of their work and activities ;

Last , Continue to pass on their estimates to the next level of Management , Until the grass-roots personnel of the project .

Scope of application : Previous projects for analogy are very similar in form and substance ; When the project information is difficult to obtain ( Little mastery of project details ).

advantage : It's easy , Less time-consuming 、 Low cost .

shortcoming ( limitations ): Due to the uniqueness of the project , The estimation accuracy of this method may be low .

2.2 Parameter estimation method

Parameter estimation is the use of historical data and other variables ( For example, the square meter cost during construction , Number of coding lines in software programming , Required man hours , Function point method in software project estimation, etc ) The statistical relationship between ,

An estimation technique to calculate the cost of activity resources . The accuracy of this technical estimation depends on the complexity of the model and the amount of resources and cost data involved .

2.3 Reserve analysis

Emergency reserve

Emergency reserve : Many cost estimation experts are used to adding provisions or contingency reserves to the cost estimation of planned activities . Emergency reserve is the estimated cost freely used by the project manager , Used to deal with expected but uncertain events , These events are called “ Known unknown events ”, Is part of the project scope and cost baseline .

Manage reserves

Manage reserves : Planned for the future , But the budget reserved for possible cost changes . Not part of the cost benchmark , Used for processing “ Unknown unknown events ”.

The difference is shown in the table below

2.4 Bottom-up estimating

Bottom-up estimating : It is also called Bill of quantities . First, the cost of a single work package or activity is specified 、 Careful estimation ; Then report to the higher levels .

advantage : detailed 、 accuracy .

shortcoming : Time consuming 、 The cost of estimating itself is high .

2.5 quality cost

quality cost : Quality cost considerations and assumptions .

The cost of prevention : Prevent non conformance ( train );

Evaluate costs : The cost of evaluating to ensure compliance ;

rework ( Failure ) cost : Rework and repair 、 guarantee .

The first two items are consistency costs .

2.6 Seller's bid analysis

Seller's bid analysis : According to the bidding situation of the qualified seller , Analyze project cost .

3、 Estimated cost output

3、 ... and 、 Budget making

Cost budget : Aggregate estimated costs for all individual activities or work packages , To establish a cost benchmark .

1、 Comparison between cost estimate and cost budget

2、 Budget making — Tool technology

2.1 Cost summary

explain : The cost base includes contingency reserves but does not include management reserves ; The project budget includes management reserves .

2.2 Historical relations

Historical relations : There may be some historical relationships between relevant variables that can be used for parameter estimation or analogy estimation . Based on these historical relationships , Use project features ( Parameters ) To build a mathematical model , Forecast the total cost of the project .

2.3 Capital limit balance

Capital limit balance : Should be based on any restrictions on project funding , To balance capital expenditure . If you find a difference between the capital limit and the planned expenditure , The work schedule may need to be adjusted , To balance the level of capital expenditure . This can be achieved by adding mandatory dates to the project schedule .

3、 Output — Cost basis

Cost baseline ( Also called cost benchmark ) It is a time phased budget used to measure and monitor project cost performance . Usually, the S Curve form display . When to plan how much to spend , It is the scale of cost in time .

A project ( Especially big projects ) There can be multiple cost benchmarks , To measure all aspects of project cost performance . For example, expenditure plan or cash flow forecast is the cost benchmark for measuring expenditure ; In large projects , Management may require the project manager to monitor internal costs separately ( artificial ) And external costs ( Contractor's cost ) wait , Multiple baselines can be set .

3.1 Project cost budget table ( Cost basis )

explain : Total project budget = Cost basis + Manage reserves

Total capital requirements = Cost basis + Manage reserves

The project budget and fund demand amount are equal , The former is S curve , The latter is ladder like .

Four 、 cost control

cost control : Monitor project status , To update project costs : The process of managing cost baseline changes .

1、 cost control — Tool technology

1.1 Earned value management

Earned value management : It is a comprehensive range 、 Time 、 Methods of cost performance measurement . The workload will be planned 、 The actual cost is compared with the income of the actual earned value , Determine whether the cost and schedule are implemented as planned .

2、 Example of earned value calculation

1、 scene

For general planning 10 Tianzhong 100 A tree , The completion budget is 10000 element ;

The specific plan is to plant... Every day 10 star , The budget for each tree is 100 element , Spend every day 1000 element ;

2、 Now it's number one 5 The day is over , Budget and implementation :

According to the plan 50 A tree , Spending budget 5000 element ;

Actually planted 30 A tree , It actually cost 4500 element .

| The term | explain | give an example |

|---|---|---|

| Completion budget BAC | Project completion budget ( Without management reserves ) | Planning use 10 Tianzhong 100 A tree , The completion budget is 10000 element |

| actual cost AC | Actual cost of work done | Actually planted 30 A tree , The actual cost 4500 element |

| Plan value PV | The planned value of the work to be done | The first 5 The day is over , According to the plan 50 A tree , Spending budget 5000 element |

| Earned value EV | The planned value of the work actually done ( Approved budget value of completed work ) | Planted 30 A tree , It is planned to cost =30*100 element =3000 element ( Actually planted 30 A tree , According to the plan, a tree costs 100 element ) |

| Schedule deviation SV | EV-PV: Less than 0, Behind schedule ; Greater than 0 Ahead of schedule | EV3000 element -PV5000 element , Less than 0, Behind schedule |

| Progress performance index SPI | EV/PV: Less than 1, backward ; Greater than 1, advance | 3000/5000, Less than 1, Behind schedule |

| Cost deviation CV | EV-AC: Less than 0, Cost overruns ; Greater than 0, Cost savings | EV3000 element -AC4500 element , Less than 0, Cost overruns |

| Cost performance index CPI | EV/AC: Less than 1, Overspending ; Greater than 1, save | 3000/4500, Less than 1, Cost overruns |

| to complete performance index TCPI | Achieve the efficiency to be maintained according to the plan :TCPI=(BAC-EV)/(BAC-AC) The efficiency to be maintained by the current completion estimate : TCPI=(BAC-EV)/(EAC-AC) | Greater than 1 Difficult to accomplish equals 1 Just finished less than 1 It's easy to do |

| ETC( Atypical ) | The completion of the project needs to be estimated ( Atypical / Special circumstances of the original budget , It won't happen again , Just planting trees is not skilled , Not in the future ):ETC=BAC-EV | ETC=10000-3000=7000 |

| ETC ( A typical ) | The completion of the project needs to be estimated ( Typical , Not in special circumstances , There will always be , For example, the ground is hard to open Ken ):ETC=(BAC-EV)/CPI | ETC=(10000-3000)/0.6667≈10499 |

| ETC ( Dual effects ) | SPI and CPI At the same time influence :ETC=(BAC- EV)/(CPI*SPI), It can be set according to actual conditions SPI and CPI The weight of | ETC=(10000-3000)/(0.6667*0.6)≈17499 |

| ETC ( re-calculate ) | ETC, There is something wrong with the estimate , Re estimate | There is a problem with the early estimation , Manual revaluation |

| EAC | Completion estimate :EAC=AC+ETC Or a quick formula for typical cases :{EAC=BAC/CPI} | EAC=4500+7000=11500( According to the atypical situation ) ;EAC=4500+10499=14999( As a typical case ) |

| Total completion time forecast | Supplementary knowledge : Planned total construction period /SPI ( A typical ); Atypical : The actual construction period that has occurred + Planned remaining duration | The original planned construction period 10 Months , at present SPI by 0.5, Then the predicted completion period =10/0.5=20 |

| VAC Deviation from completion | The difference between the completion budget and the new completion estimate :VAC=BAC-EAC | VAC=BAC-EAC |

explain :

The advantages of earned value technology : If you only look at the budget and actual expenses , There seems to be no overspending , because AC4500 It seems less than PV5000, But in terms of scope , Actually, it's overspending : Planted 30 A tree , According to the plan, it should take 3000 element , But it actually took 4500 element (EV<AC ).

Three reference rules for Earned Value Management estimation

There are three ways to estimate the implementation value of a work package (EV) The law of :

0-100: The most conservative . Only when it is completely completed will it be recorded as completed .

100-100: The most aggressive . As long as the work starts, it is recorded as done .

50-50: frequently-used . Remember to finish the work at the beginning 50%, Write it down after the work is finished 50%( Another kind of view : Remember to finish the work at the beginning 50%, Over work 50% Remember to complete ) .

Description of schedule deviation and cost deviation

Less than is not a good thing (SV、CV Less than 0, or API、CPI Less than 1): Behind schedule , Cost overruns

Greater than is a good thing (SV、CV Greater than 0, or API、CPI Greater than 1): Ahead of schedule , Cost savings

Is full of EV start

边栏推荐

猜你喜欢

How to check the frequency of memory and the number of memory slots in CPU-Z?

Two position relay xjls-8g/220

Implementation of easyexcel's function of merging cells with the same content and dynamic title

![Navigation [machine learning]](/img/79/8311a409113331e72f650a83351b46.png)

Navigation [machine learning]

多线程基础部分Part3

Kubesphere cluster configuration NFS storage solution - favorite

JVM的垃圾回收机制

C语言练手小项目(巩固加深知识点理解)

竣达技术丨多品牌精密空调集中监控方案

Leetcode298 weekly race record

随机推荐

1317. convert an integer to the sum of two zero free integers

Dev++ environment setting C language keyword display color

How win 10 opens the environment variables window

项目-h5列表跳转详情,实现后退不刷新,修改数据则刷新的功能(记录滚动条)

竣达技术丨多品牌精密空调集中监控方案

Webrtc Series - Network Transport 7 - ice Supplement nominations and ice Modèle

Small program of C language practice (consolidate and deepen the understanding of knowledge points)

Comprehensive application of OpenCV in contour detection and threshold processing

30 SCM common problems and solutions!

Multithreading basic part part 1

[collection] Introduction to basic knowledge of point cloud and functions of point cloud catalyst software

427-二叉树(617.合并二叉树、700.二叉搜索树中的搜索、98. 验证二叉搜索树、530.二叉搜索树的最小绝对差)

Logu p4683 [ioi2008] type printer problem solving

资深【软件测试工程师】学习线路和必备知识点

Wholestagecodegen of spark

30个单片机常见问题及解决办法!

Junda technology - centralized monitoring scheme for multi brand precision air conditioners

Implementation of easyexcel's function of merging cells with the same content and dynamic title

Two position relay xjls-8g/220

Functional continuous